China & the Fed: Blowing Bubbles

The race to reflate is forcing stocks, commodities and Gold Bullion higher even as the world economy slows...

EVER SINCE THE historic stock-market crash of October 1987, the Federal Reserve has responded to every recession in the US economy by slashing interest rates and funneling massive amounts of money into the hands of Wall Street's aristocracy, reports Gary Dorsch of Global Money Trends.

This ruling class dominates the two political parties in Washington. And the Fed's cash injections have usually found their way into assets, including commodities, stocks, and mortgage-backed securities, and often fueling speculative binges into stratospheric heights.

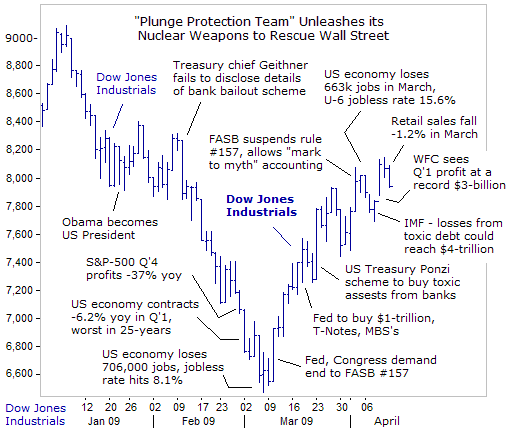

But on March 12th of 2009, US President Barack Obama warned a group of chief executive officers of the Business Roundtable that the Fed "can't continue with its policies of endless cycles of bubble and bust, and instead, must build a new foundation for future economic growth."

Obama blamed the lingering banking crisis on "reckless speculation and spending beyond our means, on bad credit, inflated home prices, and over-leveraged banks. Such activity isn't the creation of lasting wealth. It's the illusion of prosperity, and it hurts us all in the end," Obama warned.

"We cannot settle for a return to the status quo. We must put an end to the reckless speculation, spending beyond our means; bad credit, over-leveraged banks, and the absence of oversight that condemns us to bubbles that inevitably bust," Obama added.

Yet only a few days earlier, Obama exerted maximum pressure on the Financial Accounting Standards Board (FASB) to let Wall Street bankers set their own prices for toxic assets in earnings reports, regardless of market prices.

By suspending the so-called "mark to market" accounting rules, concerning the value of toxic securities they hold, FASB's new guidance would allow American banks to value assets using their own internal "mark-to-myth" models. This is, in fact, is the creation of a loophole allowing bankers to conceal their true losses and cook their financial books. By allowing the banks to claim their assets as fundamentally sound, the ruling elite expect the panic selling in the stock market will subside, banks will start lending again, and the US economy will gradually recover.

So far, all the measures taken by Obama's economic team in response to the financial crisis, have pointed their aim at protecting the wealth of the Wall Street aristocrats. Treasury Secretary Geithner announced a scheme to enable the banks to offload their toxic assets by subsidizing hedge funds and private-equity firms to purchase them at inflated prices, using hundreds of billions of taxpayer money to cover any losses, and insure double-digit profits for the speculators.

The masters of Wall Street erupted into great euphoria and jubilation over the death of FASB #157, as well as Geithner's scheme to loot taxpayer funds and offload the toxic assets of the financial oligarchs, creating the illusion of new-found wealth.

Obama himself went a step further to reassure the Wall Street titans, by quietly killing a bill passed by the House of Representatives that would have taxed 90% of the bonuses of wealthy executives and traders at AIG and other bailed-out firms.

By obscuring the accuracy of bank balance sheets, mixed with the Fed's zero-percent interest rate policy, and the hallucinogenic "Quantitative Easing" drug, traders are taking collective leave of their senses, succumbing to delusions of ever-expanding wealth, and actively participating in the creation of new bubbles. And by definition, market bubbles can expand much farther than most traders can imagine.

Nobody bothered to ask how Wells Fargo (WFC) could post a record $3 billion profit in the first quarter, at a time when one in eight US homeowners with mortgages are behind on their loan payments or in the foreclosure process.

Job losses intensify, and California home prices are 40% below their peak levels. Yet operating under the illusions of "mark-to-myth" accounting, and the hallucinogenic "QE-drug" – administered by the Fed – hedge-fund traders accepted the Wells Fargo earnings report at face value, bidding its share price 30% higher.

Former Fed chief "Easy" Al Greenspan and his protégé, Ben "Bubbles" Bernanke, hold the view that deliberate bubble-bursting is something between impossible and dangerous, and thus is best avoided. The Fed is inherently opposed to hiking interest rates, to prevent bubbles from arising in the first place.

Instead, the Fed allows stock market bubbles to inflate into the stratosphere, and patiently waits for the bubbles to burst under their own weight. Afterwards, the Fed moves to cushion the meltdown, by slashing interest rates and flooding the banking system with liquidity – the infamous Bernanke/Greenspan Put.

The Fed operates under the belief that wealth in an asset-based economy is created by massively inflating the money supply and pumping-up the value of financial or tangible assets. Today, the Fed has joined the Bank of England and the Bank of Japan in printing trillions of British Pounds, Yen and US Dollars under the radical "Quantitative Easing" framework, designed to monetize their respective government's debt, which in part, is used to bail-out the financial aristocracy.

And meantime in China...?

Central bankers inflate bubbles in order to give households a fresh sense of wealth, encouraging them to borrow and spend more, and businesses to boost investments. The strategy is built around the massive expansion of the money supply.

There are generally two types of bubbles. Firstly, speculative excesses are fueled by irresponsible bank lending. The second type of asset bubble is one in which bank lending plays a minor or no role at all, and it's usually related to the introduction of new technology or rapid industrialization that promises untold riches.

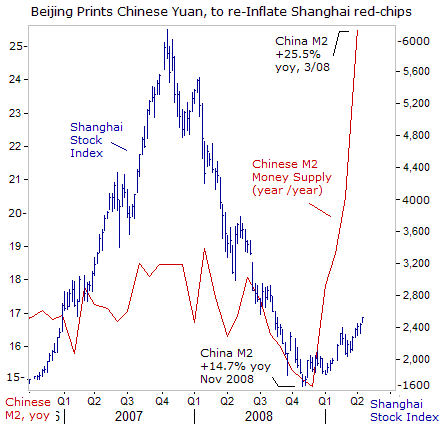

The Nasdaq high-tech stock bubble is an example of this second type. So was the spectacular run-up in the Shanghai red-chip index, which soared four-fold in 2007, mirroring China's rapid accession as the world's third largest industrial power and the biggest exporter.

China's vast manufacturing sector still employs tens of millions of workers and functions as the cheap labor workshop for Asian and Western companies, and is the biggest customer for Australian and Brazilian miners. But after the collapse of red-chip prices, it's the first type of bubble which Beijing is now busy inflating today, with the ruling Politburo ordering its state-owned banks to lend Yuan aggressively.

China's central bank said on April 12th that it will ensure massive liquidity to sustain economic growth, squashing speculation that regulators might try to restrain bank lending which could lead to bad debts and asset bubbles. Hence in March alone, Chinese banks extended 1.9-trillion Yuan in local currency loans, bringing the first-quarter total to 4.6 trillion Yuan, ($585bn), larger in size than Beijing's 4 trillion Yuan fiscal spending plans.

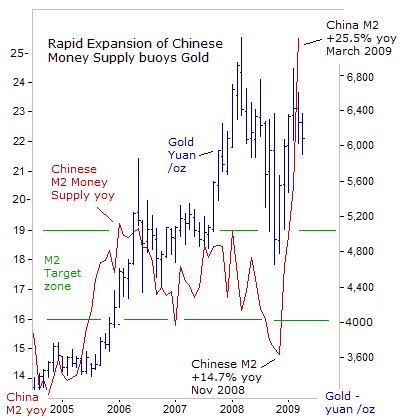

In turn, explosive lending in China has fueled the explosive expansion of the Chinese M2 money supply, now standing 25.5% higher than a year ago, thanks to its fastest growth rate in 12 years. With the blessing of Beijing, much of this money is funneled into Shanghai equities and the property markets, thereby inflating prices. The combined fiscal and monetary stimulus, equaling about 30% of China's GDP, is widely expected to lift the local economy out of its deep slump, through the traditional strategy of inflating market bubbles and indirectly boosting household wealth.

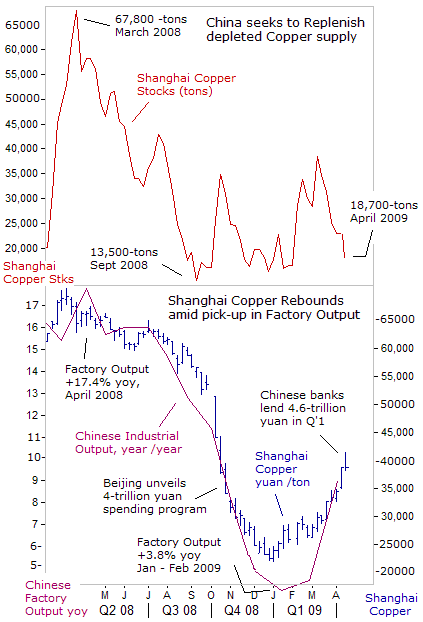

Indeed, China's industrial output rebounded to an annualized 8.3% growth rate in March, up from a record low of 3.8% in the first two months of the year, adding to evidence that Beijing's stimulus plans are starting to take effect.

Even so, China's factory sector is structurally dependent on exports, and therefore it remains highly vulnerable to any downturn in foreign demand, which is beyond Beijing's control.

In fact, the spectacular growth of China might not have been possible without the massive expansion of household debt in the United States. But this growth of debt, which sustained the US economy and global demand for 15 years, is now de-leveraging and morphing into the biggest banking crisis since the 1930s. As a result, China's vast export machine is grinding to a halt. Without the government's stimulus measures, the predicted growth rate for China would be closer to 2% this year.

So far, however, some of the big winners from China's massive stimulus plans are skilled operators in copper futures and base metal miners. Copper stockpiling by the secretive Chinese Reserves Bureau is rumored to reach 300,000 tons this year. China's imports of the red metal jumped 71% to 451,400 tons in the first two months from a year ago, customs data showed. And on the Shanghai Futures Exchange, copper futures are up 85% above December's lows. Meanwhile, copper inventories in Shanghai warehouses have dropped to dangerously low levels at 18,766 tons, prompting a fresh wave of arbitrage buying in London.

China is also riding to the rescue of the American farmer. In Chicago, soybean futures have jumped 15% over the past four-weeks, to $10.35 per bushel, whetted by China's voracious appetite. Beijing confirmed that it bought 3.86 million tons of soybeans in March, up 66% from a year earlier, and the second highest monthly tally ever.

More than half of this week's US exports, some 10.4-million bushels, are headed to China. This comes at a time when US soybean stockpiles are projected to reach a five-year low of 165 million bushels this summer.

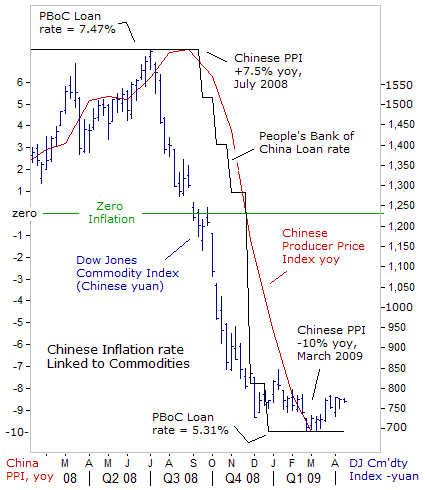

The PBoC is engineering a vast expansion of money and credit to bolster its economy, and taking advantage of a narrow window of opportunity – the collapse of factory-gate inflation, which is 10% lower than a year earlier.

The stunning collapse of a broad array of commodity prices, including crude oil, gasoline, kerosene, diesel, base metals, food and clothing, provides the necessary cover for the PBoC's massive money printing operations – which are of course the traditional antidote for warding-off deflation.

The People's Bank of China last cut its key one-year lending rate to 5.31% on Dec 22nd, still much higher in inflation-adjusted terms than those pegged by the other G7 central banks. The PBoC has cut rates five times since September and reduced bank reserve requirements four times. It has also abolished credit quotas, triggering a surge in bank lending in support of the government's 4 trillion Yuan fiscal stimulus package.

With its command and control over the Chinese banking network, the PBoC has demonstrated its ability to burst bubbles in the Shanghai stock market. That's what it did last year, hammering the red-chip index 75% below its October 2007 peak. But now, the PBoC is printing money at a feverish pace, to re-inflate the stock market.

Endorsed by Premier Wen Jiaboa, the aim is to reflate China's economy onto the road to recovery. But what is involved here is an attempt to equate a rising stock market with economic recovery, even as unemployment continues to rise, and exports fall.

So far, China's lending boom and efforts to re-inflate the Shanghai red-chip bubble has coincided with its stockpiling of copper and soybeans. The Shanghai Index closed at 2,513 points – it's highest since August, with over thirty Shanghai-A shares soaring by their 10% daily-limit – is a sign that speculators, brimming with cheap bank loans, are returning to the roulette-table.

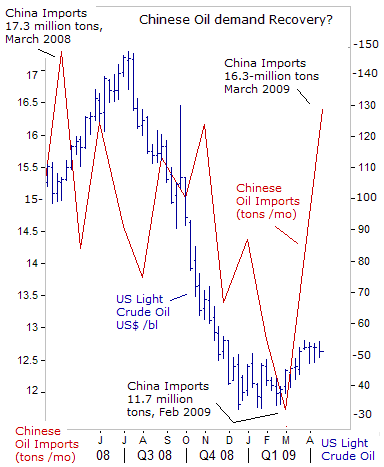

Wuhan Steel and China Cosco both leapt 10%, as strong economic data configured by Beijing's apparatchik's stirred optimism. But trade data released on April 10th was also of great interest to Nymex oil traders, with China importing 16.3 million tons of crude in March, up 33% from February's 11.7 million tons.

According to a three-year plan designed by the National Energy Administration, China's stimulus plan would include building large oil and natural gas refineries, increasing its total oil refining capacity to 440 million tons by 2011, which might also be a prelude to national stock building of energy fuel.

But optimism for a Chinese-led crude oil rally, was delayed by an IEA report, predicting that world oil demand would fall 2.4-million bpd to 83.4 million bpd in 2009, the biggest annual contraction since the early 1980's. Chinese demand for crude oil is expected to fall 1% this year, the first decline in decades. By all indications however, the IEA's estimate of future oil demand is probably off-the mark, judging by the failure of OPEC to jig the market higher.

OPEC agreed on March 15th to keep output quotas unchanged, as part of its effort to help mend the world economy.

"We believe the global economy is still very weak," noted Qatar's Abdullah al-Attiyah on March 30th. "The crisis has not reached the bottom so we have to be very careful. We are saying that $40-to-$50 per barrel is more pragmatic for the economic crisis. We cannot do more than that, but it doesn't mean we are going to cut production in May," he hinted.

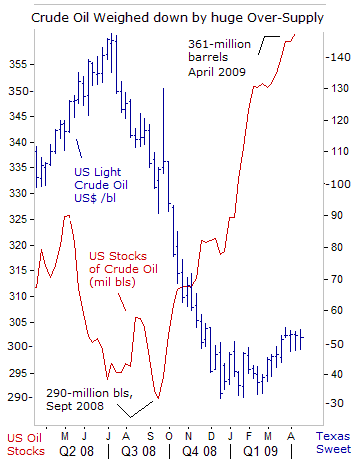

US inventories of unsold crude oil are bloated at 361 million barrels, their highest levels since July 1993, weighing down on oil prices. US oil demand in January was 989,000 bpd less than a year earlier, tumbling to 19.1 million barrels per day. In Japan and Korea, the world's third and fifth largest energy importers, crude inventories have also risen due to the worst recession since WWII.

So in explaining oil's recent rebound from $35 per barrel to around $52 per barrel today, Qatar's al-Attiyah simply said that "The current oil price is not related to demand and supply. It is higher mainly because of a weak US Dollar."

So while Beijing is calling on the G-20 to replace the US Dollar as the world reserve currency, meantime, the Chinese central bank is simultaneously printing vast quantities of Yuan.

And the rapid expansion of Chinese M2 is buoying Gold Prices in Shanghai, since the Chinese Yuan has no intrinsic value whatsoever, but for the fact that it has been decreed as legal tender.

Chinese traders confronted with limited choices, are also bidding up Shanghai red-chips, even at a time when industrial profits were 37% lower in the first quarter compared with a year ago. Traders are intoxicated by bubble-mania, and acting out of fear of the inflationary impact of the PBoC's printing press.

Shanghai gold traders are waiting to find out if Obama's economic team will label Beijing as a currency manipulator, in the next semi-annual US Treasury Department report. "I recognize that China's currency manipulation and domestic subsidies give it an unfair trade advantage and has led to US- job losses. I am committed to tackling this problem and ensuring that all trade manipulations are addressed by the US government," Obama said rhetorically ahead of the Nov 4th election.

But given America's desperate fiscal condition, Obama needs to convince China to keep investing its foreign exchange reserves in US Treasuries in order to help finance the bailout of failing US-banks and pay for the $787 billion US stimulus package. Yet China's financial security is increasing intertwined with US Treasury bonds, which are fast becoming a risky option, inflated within a bubble of gigantic proportions. It will be too late to leave the game of musical chairs, when China and Japan decide to stop buying or begin selling the US Treasury bonds.

Someday, Beijing might take pre-emptive action to Buy Gold directly from the IMF to re-balance its portfolio.

Email us

Email us